Some mostly decent numbers.

Consumer Sentiment slid back a few over concerns of a "Wave 2". I felt the previous reading may have been a bit too optimistic.

Inventories took a couple steps back, in May.

Jobless claims remain high and the reduction last week was barely a blip. A major point of concern for me. Thankfully Job Openings continue to edge up but remain well below current unemployment levels. (A Dynamic not seen since 2009).

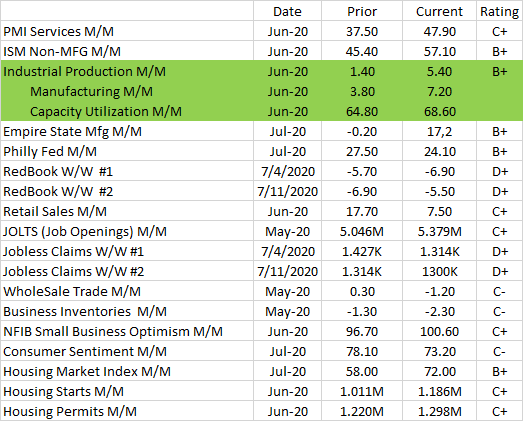

PMI Services earned a C+ which is somewhat of a break from my typical grading as it remains slightly negative (Below 50), but it had a 10 point gain over the previous reading. Couple that with the more notable ISM gain to a massive 57.1, and the Service Sector, which makes up a lions share of the economy (Roughly 60%), is looking strong.

Small Businesses are back to pre-Covid levels of optimism as are the Home Builders as measured by the Housing Market Index..

Speaking of Housing, Starts and Permits are both up nicely which is likely to add a bump to the upcoming Leading Indicators and GDP Forecasts.

RedBook remains soft but Retail Sales remain strongly positive in growth.

MFG remains on fire based on Empire State and Philly Fed and most notably Industrial Output. I combined MFG and Capacity Utilization as they are sub-metrics of Industrial Production and I wanted to report them while not Skewing the weeks Grade.

I'm comfortable with a C+ this week but the GDP Forecats and Jobless Claims keep the suck factor at a solid 8.

Hiya Cw. I was wondering what you thought of the housing numbers? They look pretty good from this side of the computer.

Great work Tim!

This must be an especially challenging endeavor with historical changes in all the metrics going back to the start of the pandemic.

For perspective(and to appreciate your hard work).

I went back and took a snap shot of some of your previous work.

Reports from March, April, May and June to compare with July.

metmike: Nothing but C grades below.............as we hit the start of the pandemic affects.

https://www.marketforum.com/forum/topic/49254/

By TimNew - March 21, 2020, 1:56 p.m.

One more test

| Date | Prior | Current | Rating | |

| Empire St Mfg M/M | Mar-20 | 12.9 | -21.5 | C- |

| Retail Sales M/M | Feb-20 | 0.30% | -0.50% | C- |

| Redbook W/W | 3/14/2020 | 6.00% | 8.50% | C+ |

| Industrial Production M/M | Feb-20 | -0.30% | 0.60% | C+ |

| Business Inventories M/M | Jan-20 | 0.10% | -0.10% | C |

| JOLTS (Job Openings) M/M | Jan-20 | 6.432M | 6.963M | C+ |

| Housing Maket Index M/M | Mar-20 | 74 | 72 | C |

| Housing StartsM/M | Feb-20 | 1.567M | 1.599M | C+ |

| Permits | Feb-20 | 1.551M | 1.464M | C- |

| Existing Home Sales | Feb-20 | 5.46M | 5.77M | |

| Jobless Claims W/W | 3/14/2020 | 211K | 281K | C- |

| Philly FedM/M | Mar-20 | 36.7 | -12.7 | C- |

| Leading Indicators M/M | Feb-20 | 0.8 | 0.1 | C |

Much nicer presentation. Align all cels horizontally centered.

Anyway, I think any Metric from Feb or before should have an * as we know dynamic economic changes have recently taken place.

Notable in the last week was the 70k jump in Unemployment claims. I expect further increases. The severity will depend on further virus news.

Also notable was the drop in Empire State Mfg. A regional report, and far from the most significant MFG Metric, but likely along with Philly Fed, an indicator of things to come. Dallas MFG is largely tied to energy and should also take a hard hit in the next report. The rest? We'll see, but I am not optimistic.

Interesting that Redbook showed an increase in retail; Likely due to hoarding?

It's really difficult to form an overall conclusion with the current data we have so far.. Needless to say, strength in metrics, going forward, would be a pleasant but unlikely surprise. For now, I'll give the week a C- as we are likely seeing an economy in contraction. The question is what severity.

https://www.marketforum.com/forum/topic/50714/

Started by TimNew - April 17, 2020, 10:57 a.m.

| Date | Prior | Current | Rating | |

| NFIB Small Business Optimism M/M | Mar-20 | 104.50 | 96.40 | C- |

| RedBook W/W | 4/4/2020 | 6.30% | 5.30% | C |

| Job Openings (JOLTS) M/M | Feb-20 | 6.953M | 6.882M | C |

| Consumer Sentiment M/M | Apr-20 | 89.10 | 71.00 | C- |

| RedBook W/W 1 | 4/4/2020 | 6.30% | 5.30% | C |

| RedBook W/W 2 | 4/11/2020 | 5.30% | -2.00% | C- |

| Jobless Claims W/W 1 | 4/4/2020 | 6,648K | 6608K | F+ |

| Jobless Claims W/W 2 | 4/11/2020 | 6608K | 5245K | F+ |

| Retail Sales M/M | Apr-20 | -0.50 | -8.70 | C- |

| Empire State Mfg M/M | Apr-20 | -21.5 | -78.2 | D+ |

| Philly Fed Bus Outlook M/M | Apr-20 | -12.7 | -56.6 | D- |

| Industrial Production M/M | Mar-20 | 0.5 | -5.4 | C- |

| Housing Market Index M/M | Apr-20 | 72 | 30 | D |

| Housing Starts M/M | Mar-20 | 1.599M | 1.216M | C- |

| Housing Permits M/M | Mar-20 | 1.464M | 1.353M | C- |

| Leading Indicators M/M | Mar-20 | 0.1 | -6.7 | D- |

As the reports catch up, the number look worse and worse, and I doubt anyone is surprised.

Leading Indicators just came out with the worst reading in the history of the metric. The DOW shed 200 point right after it's release tho it remains positive on hopes of reopening and promising treatment data. I went with a D- to leave room to the downside. Housing Permits have a strong impact and I think they will get worse before they get better.

Retail is finally taking a major hit which may be the worst news we've seen so far. Consumer Sentiment is showing why with a drop to 71.

Small Business Optimism took a hit tho remains stronger than I would have expected. Stimulus Checks?

Industrial Production, Empire State and Philly Fed all took a significant hit.

Jobless Claims have improved but it's hard to look at 5+ million as good news, even when compared to 6+ million.

Housing Numbers (Starts/Permits) saw a reduction but the Housing Market Index, which is really a survey of builders came in with the lowest reading I've ever seen @ 30, suggesting we'll see much worse in the base housing numbers.

I'm of the opinion that we have not yet seen long term effects on the overall economy, but possibly a few more weeks like this, certainly as month, and we will be in a hole that will take some serious climbing to escape. Based on that. I'll go with an overall D- and hope I am not being too optimistic.

Week in Review

2 responses | 0 likes

https://www.marketforum.com/forum/topic/52615/

Started by TimNew - May 22, 2020, 7:29 a.m.

Nothing of consequence being reported today and I have a busy weekend coming up, so off we go.

Note: I;ve excluded the PMI Composite Flash, key word being "Flash". I'll include the more comprehensive full report which will be released next week. I gave it an honorable mention earlier.

Again with no real surprise this week:

Retail showed an increased decrease this week. I do find this a little dissapointing as I expect we'll be seeing better (not good) numbers in the near term. I also expected E-Commerce to take a larger slice than it did as Amazon, et.al. have been going full blast+. Perhaps next QTR? Q1 was on the cusp Needless to say, people will continue to rely more and more on internet shopping. I also expect Retail will be one of the earliest signs of recovery.

Jobless claims continue to measure in the millions but continue to drop at significant rates. That well has to go dry, hopefully sooner than later. The impact remains largely in the lower income brackets.

Housing is in the ditch with a slight ray of hope in the Housing Market Index which showed an uptick of 7 points. This is a good leading indicator as it's a survey of Builders. Of course, it still remains at about half of the low normal.

Philly Fed and Leading indicators trimmed their descent but remain in historically low territory.

Overall, the trend is "Not as bad as it was".. Still abnormally bad, just not quite as abnormally bad. I continue to hold optimism for the not too distant. I'll give the week a well earned D+.

https://www.marketforum.com/forum/topic/54652/

Week in Review

9 responses |

Started by TimNew - June 27, 2020, 8:43 a.m.

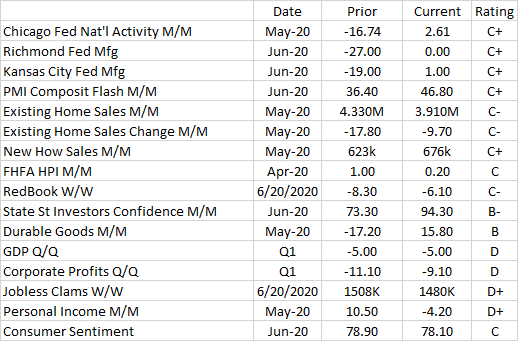

Somewhat mixed this week, but I see encouraging signs.

Personal Income took a big hit in May. Not surprising with jobless claims remaining at about 1.5 million. The decrease in New Claims is slower than I'd like to see. Hopefully see significant drops in the not too distant.

Q1 GDP and Corporate Profits are negative, but that's no surprise. Q2 may look worse.

Existing Homes sales slowed their decent but remain strongly negative, somewhat offset by a healthy bump in New Home Sales.

Redbook remains negative, but as mentioned, it's a subset of retail and On-Line is booming as the streets remain crowded with assorted delivery trucks.

Consumer Sentiment is steady at historically low levels yet State Street Investors mirror my opinion as their confidence showed a significant improvement.

Chicago, Richmond and Kansas City Fed all showed marked improvement as did the PMI Flash.

The most encouraging news this week for me is in Durable Goods which showed nothing short of a remarkable turnaround in May.

As stated, a somewhat mixed week but slightly positive IMO. I'll go with a C+ largely weighted with the Durable Goods. Suck Factor remains at 8 with the Jobless Claims remaining in the Stratosphere.

Tim we had a 3 month back log before the CCP virous. We worked right through the shut down. ( had 2 employees that off for 2 weeks, they thought were going to collect unemployment). We still have a back log of 3 to 4 weeks. Note : we only have 5 employees

There is a lot of interest in new homes.

My daughter put her house up for sale and 2 days later had 3 offers higher than asking price. There is no supply of existing homes, causing there to be less sales. So people are looking at new housing. JMHO

Builders are not building speck houses as they are busy with sold homes. Back just before the housing crash builders were all building speck houses. In my opinion this is good.

I confess that I thought we would be in trouble but that has not happened, at least not yet.

Thanks Mike. What a long strange trip it's been :-)

And thanks CW. I really like hearing from folks in the trenches. I look from a great distance :-)